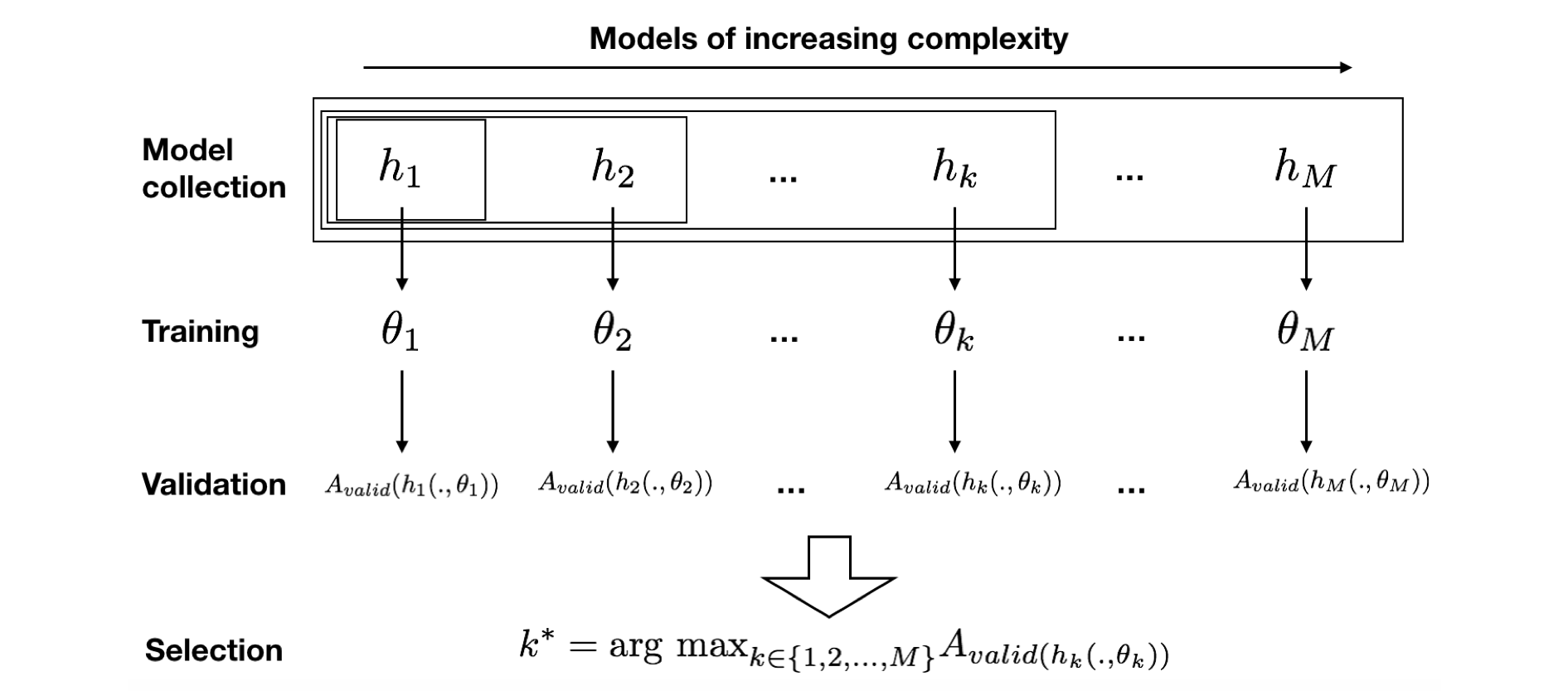

3. Model selection¶

Model selection consists in selecting the prediction model that is expected to provide the best performances on future data. The standard methodology consists of four main steps [Bis06, Bon21, FHT01]:

Define a collection of candidate models to be tested. Let \(M\) be the number of models, and \(h_k\), \(1 \le k \le M\), be the \(k-\)th model in the collection, parameterized by a set of parameters \(\theta_k\) (also see section Baseline methodology - Supervised learning). Given a class of models (such as decision trees, logistic regression, …), a common practice is to define a collection of models of increasing complexity (tree depth for decision trees, regularisation coefficients for logistic regression, …).

Train each candidate model using the training data. The training of model \(h_k\) identifies the parameters \(\theta_k\) that maximizes the performances of \(h_k\) on the training set.

Assess the performances of each candidate model by means of a validation procedure (see section Validation Strategies). The validation procedure provides an estimate of the generalization performance. Let us denote by \(A_{valid}(h_k(.,\theta_k))\) the validation performance for the \(k\)-th model.

Select the model that has the highest validation performance. Denoting by \(k^*\) the index of this optimal model, we have:

An illustration of the model selection procedure with its different steps is provided in Fig. 1.

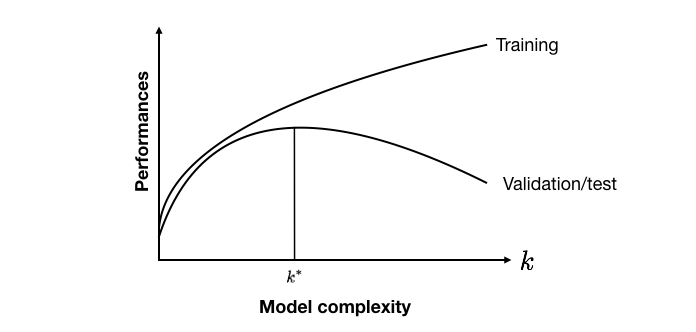

The rationale for assessing models of increasing complexity is that there is usually a trade-off between the model complexity and its generalization performances (also referred to as the bias/variance trade-off) [Bis06, Bon21, FHT01]. Models that have too few parameters fail to properly represent the relationship between input and output features (also referred to as underfitting). Models that have many parameters can perfectly represent the relationship between input and output features in the training data (also referred to as overfitting). Training data are however often noisy, and their distribution slightly different from the validation and test data. As a result, overfitting is usually detrimental to the performances on the validation or test data.

A qualitative representation of the trade-off between model complexity and performances is illustrated in Fig. 2. The training performances usually increase with the model complexity. The optimal validation and test performances are found for models of intermediate complexity, that both avoid underfitting and overfitting. This trade-off was experimentally illustrated with decision trees in the previous section on Validation Strategies.

This section aims at refining the sklearn validation pipeline, and exploring the trade-offs between model complexity and performances for different classes of models.

# Initialization: Load shared functions and simulated data

# Load shared functions

!curl -O https://raw.githubusercontent.com/Fraud-Detection-Handbook/fraud-detection-handbook/main/Chapter_References/shared_functions.py

%run shared_functions.py

# Get simulated data from Github repository

if not os.path.exists("simulated-data-transformed"):

!git clone https://github.com/Fraud-Detection-Handbook/simulated-data-transformed

% Total % Received % Xferd Average Speed Time Time Time Current

Dload Upload Total Spent Left Speed

100 31568 100 31568 0 0 83513 0 --:--:-- --:--:-- --:--:-- 83513

3.1. Model selection: Decision trees¶

Let us first reproduce the sklearn prequential validation pipeline proposed in the previous section. We load three months of transaction data, and define the output feature as the fraud label TX_FRAUD, and the inputs features as the set of features obtained from the baseline preprocessing.

# Load data from the 2018-06-11 to the 2018-09-14

DIR_INPUT = 'simulated-data-transformed/data/'

BEGIN_DATE = "2018-06-11"

END_DATE = "2018-09-14"

print("Load files")

%time transactions_df = read_from_files(DIR_INPUT, BEGIN_DATE, END_DATE)

print("{0} transactions loaded, containing {1} fraudulent transactions".format(len(transactions_df),transactions_df.TX_FRAUD.sum()))

output_feature = "TX_FRAUD"

input_features = ['TX_AMOUNT','TX_DURING_WEEKEND', 'TX_DURING_NIGHT', 'CUSTOMER_ID_NB_TX_1DAY_WINDOW',

'CUSTOMER_ID_AVG_AMOUNT_1DAY_WINDOW', 'CUSTOMER_ID_NB_TX_7DAY_WINDOW',

'CUSTOMER_ID_AVG_AMOUNT_7DAY_WINDOW', 'CUSTOMER_ID_NB_TX_30DAY_WINDOW',

'CUSTOMER_ID_AVG_AMOUNT_30DAY_WINDOW', 'TERMINAL_ID_NB_TX_1DAY_WINDOW',

'TERMINAL_ID_RISK_1DAY_WINDOW', 'TERMINAL_ID_NB_TX_7DAY_WINDOW',

'TERMINAL_ID_RISK_7DAY_WINDOW', 'TERMINAL_ID_NB_TX_30DAY_WINDOW',

'TERMINAL_ID_RISK_30DAY_WINDOW']

Load files

CPU times: user 880 ms, sys: 545 ms, total: 1.43 s

Wall time: 1.66 s

919767 transactions loaded, containing 8195 fraudulent transactions

The reference starting date for training is set at 2018-07-25, and the deltas to seven days (see Validation Strategies).

# Number of folds for the prequential validation

n_folds = 4

# Set the starting day for the training period, and the deltas

start_date_training = datetime.datetime.strptime("2018-07-25", "%Y-%m-%d")

delta_train = delta_delay = delta_test = delta_valid = delta_assessment = 7

start_date_training_for_valid = start_date_training+datetime.timedelta(days=-(delta_delay+delta_valid))

start_date_training_for_test = start_date_training+datetime.timedelta(days=(n_folds-1)*delta_test)

The performance metrics are the AUC ROC, the Average Precision, and the Card Precision@100.

# Only keep columns that are needed as argument to the custom scoring function

# (in order to reduce the serialization time of transaction dataset)

transactions_df_scorer = transactions_df[['CUSTOMER_ID', 'TX_FRAUD','TX_TIME_DAYS']]

card_precision_top_100 = sklearn.metrics.make_scorer(card_precision_top_k_custom,

needs_proba=True,

top_k=100,

transactions_df=transactions_df_scorer)

performance_metrics_list_grid = ['roc_auc', 'average_precision', 'card_precision@100']

performance_metrics_list = ['AUC ROC', 'Average precision', 'Card Precision@100']

scoring = {'roc_auc':'roc_auc',

'average_precision': 'average_precision',

'card_precision@100': card_precision_top_100,

}

For the sake of conciseness, let us define a model_selection_wrapper function, that will perform prequential validation for both the validation and the test sets.

def model_selection_wrapper(transactions_df,

classifier,

input_features, output_feature,

parameters,

scoring,

start_date_training_for_valid,

start_date_training_for_test,

n_folds=4,

delta_train=7,

delta_delay=7,

delta_assessment=7,

performance_metrics_list_grid=['roc_auc'],

performance_metrics_list=['AUC ROC'],

n_jobs=-1):

# Get performances on the validation set using prequential validation

performances_df_validation=prequential_grid_search(transactions_df, classifier,

input_features, output_feature,

parameters, scoring,

start_date_training=start_date_training_for_valid,

n_folds=n_folds,

expe_type='Validation',

delta_train=delta_train,

delta_delay=delta_delay,

delta_assessment=delta_assessment,

performance_metrics_list_grid=performance_metrics_list_grid,

performance_metrics_list=performance_metrics_list,

n_jobs=n_jobs)

# Get performances on the test set using prequential validation

performances_df_test=prequential_grid_search(transactions_df, classifier,

input_features, output_feature,

parameters, scoring,

start_date_training=start_date_training_for_test,

n_folds=n_folds,

expe_type='Test',

delta_train=delta_train,

delta_delay=delta_delay,

delta_assessment=delta_assessment,

performance_metrics_list_grid=performance_metrics_list_grid,

performance_metrics_list=performance_metrics_list,

n_jobs=n_jobs)

# Bind the two resulting DataFrames

performances_df_validation.drop(columns=['Parameters','Execution time'], inplace=True)

performances_df=pd.concat([performances_df_test,performances_df_validation],axis=1)

# And return as a single DataFrame

return performances_df

Prequential validation can now be performed with the few following lines of code, by

defining which classifier to use

defining which parameters to test

fitting the models and assessing the performances

The implementation using decision trees as predictions models, for maximum depth in \([2,3,4,5,6,7,8,9,10,20,50]\), is obtained with:

# Define classifier

classifier = sklearn.tree.DecisionTreeClassifier()

# Set of parameters for which to assess model performances

parameters = {'clf__max_depth':[2,3,4,5,6,7,8,9,10,20,50], 'clf__random_state':[0]}

start_time = time.time()

# Fit models and assess performances for all parameters

performances_df=model_selection_wrapper(transactions_df, classifier,

input_features, output_feature,

parameters, scoring,

start_date_training_for_valid,

start_date_training_for_test,

n_folds=n_folds,

delta_train=delta_train,

delta_delay=delta_delay,

delta_assessment=delta_assessment,

performance_metrics_list_grid=performance_metrics_list_grid,

performance_metrics_list=performance_metrics_list,

n_jobs=1)

execution_time_dt = time.time()-start_time

# Select parameter of interest (max_depth)

parameters_dict=dict(performances_df['Parameters'])

performances_df['Parameters summary']=[parameters_dict[i]['clf__max_depth'] for i in range(len(parameters_dict))]

# Rename to performances_df_dt for model performance comparison at the end of this notebook

performances_df_dt=performances_df

performances_df_dt

| AUC ROC Test | AUC ROC Test Std | Average precision Test | Average precision Test Std | Card Precision@100 Test | Card Precision@100 Test Std | Parameters | Execution time | AUC ROC Validation | AUC ROC Validation Std | Average precision Validation | Average precision Validation Std | Card Precision@100 Validation | Card Precision@100 Validation Std | Parameters summary | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 0.791909 | 0.017769 | 0.541761 | 0.031476 | 0.265000 | 0.019756 | {'clf__max_depth': 2, 'clf__random_state': 0} | 0.383720 | 0.790786 | 0.012035 | 0.549767 | 0.022134 | 0.256429 | 0.014481 | 2 |

| 1 | 0.809012 | 0.009125 | 0.578885 | 0.014434 | 0.281429 | 0.015940 | {'clf__max_depth': 3, 'clf__random_state': 0} | 0.425149 | 0.802717 | 0.017607 | 0.573414 | 0.027186 | 0.267143 | 0.016067 | 3 |

| 2 | 0.812555 | 0.010319 | 0.601088 | 0.020216 | 0.282500 | 0.015199 | {'clf__max_depth': 4, 'clf__random_state': 0} | 0.467093 | 0.800690 | 0.017878 | 0.554134 | 0.038293 | 0.264286 | 0.014321 | 4 |

| 3 | 0.810138 | 0.008586 | 0.600306 | 0.016797 | 0.284286 | 0.004286 | {'clf__max_depth': 5, 'clf__random_state': 0} | 0.510538 | 0.804218 | 0.016505 | 0.546094 | 0.042197 | 0.267857 | 0.013869 | 5 |

| 4 | 0.804437 | 0.007974 | 0.585132 | 0.005053 | 0.281429 | 0.007626 | {'clf__max_depth': 6, 'clf__random_state': 0} | 0.600303 | 0.798603 | 0.024225 | 0.537006 | 0.037056 | 0.264643 | 0.008474 | 6 |

| 5 | 0.782710 | 0.012483 | 0.554860 | 0.011771 | 0.268929 | 0.009813 | {'clf__max_depth': 7, 'clf__random_state': 0} | 0.664072 | 0.795636 | 0.023144 | 0.530609 | 0.040323 | 0.262500 | 0.006804 | 7 |

| 6 | 0.774783 | 0.014568 | 0.544933 | 0.003392 | 0.263571 | 0.007593 | {'clf__max_depth': 8, 'clf__random_state': 0} | 0.792020 | 0.795142 | 0.023081 | 0.516246 | 0.033545 | 0.260714 | 0.009715 | 8 |

| 7 | 0.761763 | 0.012098 | 0.520208 | 0.012309 | 0.258571 | 0.009949 | {'clf__max_depth': 9, 'clf__random_state': 0} | 0.719332 | 0.785849 | 0.026249 | 0.505189 | 0.040393 | 0.260357 | 0.009813 | 9 |

| 8 | 0.758138 | 0.011140 | 0.504909 | 0.013154 | 0.257500 | 0.010467 | {'clf__max_depth': 10, 'clf__random_state': 0} | 0.765691 | 0.786784 | 0.031165 | 0.493543 | 0.048307 | 0.257143 | 0.009949 | 10 |

| 9 | 0.754024 | 0.009848 | 0.439422 | 0.034828 | 0.261071 | 0.014335 | {'clf__max_depth': 20, 'clf__random_state': 0} | 1.195464 | 0.780408 | 0.022168 | 0.450980 | 0.031413 | 0.264286 | 0.007890 | 20 |

| 10 | 0.797225 | 0.005427 | 0.334457 | 0.020767 | 0.257857 | 0.011715 | {'clf__max_depth': 50, 'clf__random_state': 0} | 1.400485 | 0.822564 | 0.013407 | 0.341818 | 0.026227 | 0.265714 | 0.008512 | 50 |

The resulting DataFrame provides the performances in terms of AUC ROC, AP, and CP@100 for both the validation and test sets. Rows correspond to performances for a given maximum depth of a decision tree.

Let us extract from this table the most relevant information, that is, entries that allow to answer the following questions:

Which parameter provides the best performances on the validation set?

What is the performances on the test set using this parameter?

What parameter would have provided the best performance on the test set?

Answers to these questions can be organized as a table, using the get_summary_performances function.

def get_summary_performances(performances_df, parameter_column_name="Parameters summary"):

# Three performance metrics

metrics = ['AUC ROC','Average precision','Card Precision@100']

performances_results=pd.DataFrame(columns=metrics)

# Reset indices in case a subset of a performane DataFrame is provided as input

performances_df.reset_index(drop=True,inplace=True)

# Lists of parameters/performances that will be retrieved for the best estimated parameters

best_estimated_parameters = []

validation_performance = []

test_performance = []

# For each performance metric, get the validation and test performance for the best estimated parameter

for metric in metrics:

# Find the index which provides the best validation performance

index_best_validation_performance = performances_df.index[np.argmax(performances_df[metric+' Validation'].values)]

# Retrieve the corresponding parameters

best_estimated_parameters.append(performances_df[parameter_column_name].iloc[index_best_validation_performance])

# Add validation performance to the validation_performance list (mean+/-std)

validation_performance.append(

str(round(performances_df[metric+' Validation'].iloc[index_best_validation_performance],3))+

'+/-'+

str(round(performances_df[metric+' Validation'+' Std'].iloc[index_best_validation_performance],2))

)

# Add test performance to the test_performance list (mean+/-std)

test_performance.append(

str(round(performances_df[metric+' Test'].iloc[index_best_validation_performance],3))+

'+/-'+

str(round(performances_df[metric+' Test'+' Std'].iloc[index_best_validation_performance],2))

)

# Add results to the performances_results DataFrame

performances_results.loc["Best estimated parameters"]=best_estimated_parameters

performances_results.loc["Validation performance"]=validation_performance

performances_results.loc["Test performance"]=test_performance

# Lists of parameters/performances that will be retrieved for the optimal parameters

optimal_test_performance = []

optimal_parameters = []

# For each performance metric, get the performance for the optimal parameter

for metric in ['AUC ROC Test','Average precision Test','Card Precision@100 Test']:

# Find the index which provides the optimal performance

index_optimal_test_performance = performances_df.index[np.argmax(performances_df[metric].values)]

# Retrieve the corresponding parameters

optimal_parameters.append(performances_df[parameter_column_name].iloc[index_optimal_test_performance])

# Add test performance to the test_performance list (mean+/-std)

optimal_test_performance.append(

str(round(performances_df[metric].iloc[index_optimal_test_performance],3))+

'+/-'+

str(round(performances_df[metric+' Std'].iloc[index_optimal_test_performance],2))

)

# Add results to the performances_results DataFrame

performances_results.loc["Optimal parameters"]=optimal_parameters

performances_results.loc["Optimal test performance"]=optimal_test_performance

return performances_results

summary_performances_dt=get_summary_performances(performances_df_dt, parameter_column_name="Parameters summary")

summary_performances_dt

| AUC ROC | Average precision | Card Precision@100 | |

|---|---|---|---|

| Best estimated parameters | 50 | 3 | 5 |

| Validation performance | 0.823+/-0.01 | 0.573+/-0.03 | 0.268+/-0.01 |

| Test performance | 0.797+/-0.01 | 0.579+/-0.01 | 0.284+/-0.0 |

| Optimal parameters | 4 | 4 | 5 |

| Optimal test performance | 0.813+/-0.01 | 0.601+/-0.02 | 0.284+/-0.0 |

The first row provides the parameters that maximize the performances on the validation set (best estimated parameters \(k^*\)). The second and third rows provide the corresponding performances on the validation and test sets, respectively. The fourth row provides the actual optimal parameters on the test set (the parameters that maximize the performances on the test set). The fifth row provides the corresponding performances on the test set.

Two important observations can be made from this summary table. First, the optimal parameter depends on the performance metrics: It is a maximum depth of 4 for AUC ROC and AP, while it is a maximum depth of 5 for the CP@100. Second, the best parameters for the validation may not be the optimal parameter for the test set. This is the case for the AUC ROC (maximum depth of 50 for the validation set versus 4 for the test set), and the AP (maximum depth of 3 for the validation set versus 4 for the test set).

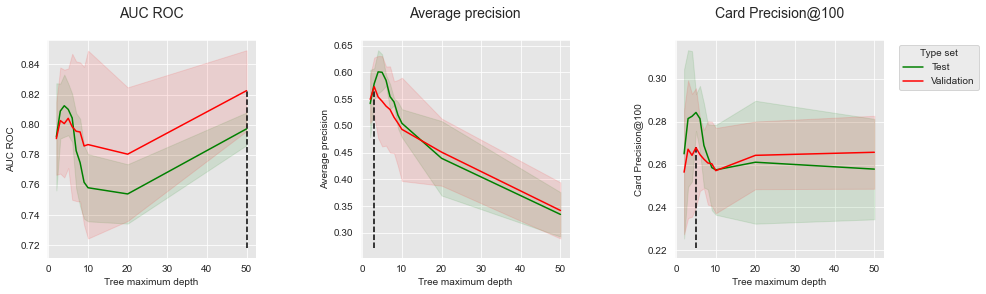

Similar to the section Validation Strategies, let us plot the performances as a function of the decision tree depth. The vertical dashed line is the tree depth for which the performance is maximized on the validation data.

get_performances_plots(performances_df_dt,

performance_metrics_list=['AUC ROC', 'Average precision', 'Card Precision@100'],

expe_type_list=['Test','Validation'], expe_type_color_list=['#008000','#FF0000'],

summary_performances=summary_performances_dt)

3.2. Model selection: Exploration of other model classes¶

This section explores the performances that can be achieved with model selection using other model classes. We cover logistic regression, random forests, and boosting (as in the section Baseline Fraud Detection System).

3.2.1. Logistic regression¶

The main hyperparameter of logistic regression is the regularization parameter C. The default value for this parameter is 1. Let us try fitting models with lower and higher values, for example in the set [0.1,1,10,100].

classifier = sklearn.linear_model.LogisticRegression()

parameters = {'clf__C':[0.1,1,10,100], 'clf__random_state':[0]}

start_time=time.time()

performances_df=model_selection_wrapper(transactions_df, classifier,

input_features, output_feature,

parameters, scoring,

start_date_training_for_valid,

start_date_training_for_test,

n_folds=n_folds,

delta_train=delta_train,

delta_delay=delta_delay,

delta_assessment=delta_assessment,

performance_metrics_list_grid=performance_metrics_list_grid,

performance_metrics_list=performance_metrics_list,

n_jobs=1)

execution_time_lr = time.time()-start_time

parameters_dict=dict(performances_df['Parameters'])

performances_df['Parameters summary']=[parameters_dict[i]['clf__C'] for i in range(len(parameters_dict))]

# Rename to performances_df_lr for model performance comparison at the end of this notebook

performances_df_lr=performances_df

performances_df_lr

| AUC ROC Test | AUC ROC Test Std | Average precision Test | Average precision Test Std | Card Precision@100 Test | Card Precision@100 Test Std | Parameters | Execution time | AUC ROC Validation | AUC ROC Validation Std | Average precision Validation | Average precision Validation Std | Card Precision@100 Validation | Card Precision@100 Validation Std | Parameters summary | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 0.866972 | 0.014858 | 0.620231 | 0.015977 | 0.297143 | 0.008207 | {'clf__C': 0.1, 'clf__random_state': 0} | 0.602494 | 0.865052 | 0.009591 | 0.608330 | 0.022740 | 0.278929 | 0.016300 | 0.1 |

| 1 | 0.867643 | 0.015404 | 0.623081 | 0.016204 | 0.297143 | 0.008806 | {'clf__C': 1, 'clf__random_state': 0} | 0.656055 | 0.866861 | 0.008988 | 0.612264 | 0.023474 | 0.278214 | 0.016914 | 1.0 |

| 2 | 0.867678 | 0.015415 | 0.623224 | 0.016087 | 0.297500 | 0.008828 | {'clf__C': 10, 'clf__random_state': 0} | 0.582498 | 0.867050 | 0.008918 | 0.612526 | 0.023715 | 0.277500 | 0.016763 | 10.0 |

| 3 | 0.867680 | 0.015419 | 0.623253 | 0.016074 | 0.297500 | 0.008828 | {'clf__C': 100, 'clf__random_state': 0} | 0.728584 | 0.867071 | 0.008912 | 0.612537 | 0.023712 | 0.277500 | 0.016763 | 100.0 |

The get_summary_performances function gives the summary of the best parameters and corresponding performances.

summary_performances_lr=get_summary_performances(performances_df_lr, parameter_column_name="Parameters summary")

summary_performances_lr

| AUC ROC | Average precision | Card Precision@100 | |

|---|---|---|---|

| Best estimated parameters | 100.0 | 100.0 | 0.1 |

| Validation performance | 0.867+/-0.01 | 0.613+/-0.02 | 0.279+/-0.02 |

| Test performance | 0.868+/-0.02 | 0.623+/-0.02 | 0.297+/-0.01 |

| Optimal parameters | 100.0 | 100.0 | 10.0 |

| Optimal test performance | 0.868+/-0.02 | 0.623+/-0.02 | 0.298+/-0.01 |

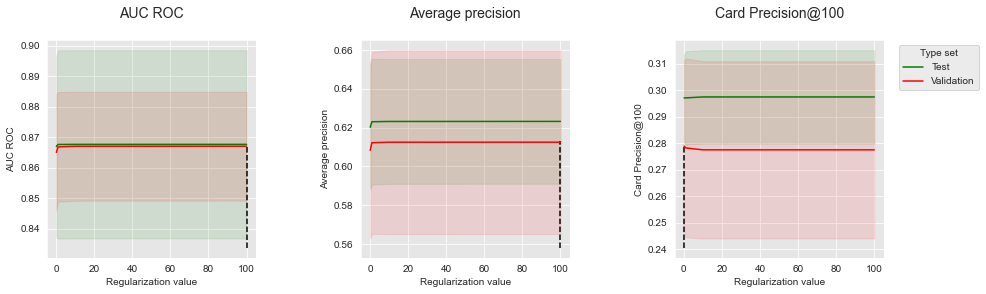

Let us plot the performances as a function of the regularization value, together with the value that provides the best estimated performances.

get_performances_plots(performances_df_lr,

performance_metrics_list=['AUC ROC', 'Average precision', 'Card Precision@100'],

expe_type_list=['Test','Validation'], expe_type_color_list=['#008000','#FF0000'],

parameter_name="Regularization value",

summary_performances=summary_performances_lr)

Performances tend to be a bit lower for a low \(C\) value (0.1). \(C\) values equal or higher than one provide similar performances. The default parameter \(C=1\) seems therefore to be a sensible value for the logistic regression model.

3.2.2. Random forest¶

The two main hyperparameters of a random forest are the maximum tree depth and the number of trees (parameters max_depth and n_estimators, respectively). By default, the maximum tree depth is None (that is, nodes are expanded until all leaves are pure or until all leaves contain less than min_samples_split samples), and the number of trees is 100. Let us try other values, by combining max_depth values in the set [5,10,20,50] and n_estimators values in the set [25,50,100].

classifier = sklearn.ensemble.RandomForestClassifier()

# Note: n_jobs set to one for getting true execution times

parameters = {'clf__max_depth':[5,10,20,50], 'clf__n_estimators':[25,50,100],

'clf__random_state':[0],'clf__n_jobs':[1]}

start_time=time.time()

performances_df=model_selection_wrapper(transactions_df, classifier,

input_features, output_feature,

parameters, scoring,

start_date_training_for_valid,

start_date_training_for_test,

n_folds=n_folds,

delta_train=delta_train,

delta_delay=delta_delay,

delta_assessment=delta_assessment,

performance_metrics_list_grid=performance_metrics_list_grid,

performance_metrics_list=performance_metrics_list,

n_jobs=1)

execution_time_rf = time.time()-start_time

parameters_dict=dict(performances_df['Parameters'])

performances_df['Parameters summary']=[str(parameters_dict[i]['clf__n_estimators'])+

'/'+

str(parameters_dict[i]['clf__max_depth'])

for i in range(len(parameters_dict))]

# Rename to performances_df_rf for model performance comparison at the end of this notebook

performances_df_rf=performances_df

performances_df_rf

| AUC ROC Test | AUC ROC Test Std | Average precision Test | Average precision Test Std | Card Precision@100 Test | Card Precision@100 Test Std | Parameters | Execution time | AUC ROC Validation | AUC ROC Validation Std | Average precision Validation | Average precision Validation Std | Card Precision@100 Validation | Card Precision@100 Validation Std | Parameters summary | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 0.845287 | 0.003872 | 0.620712 | 0.022145 | 0.289286 | 0.010570 | {'clf__max_depth': 5, 'clf__n_estimators': 25,... | 1.270088 | 0.834147 | 0.009100 | 0.610413 | 0.023740 | 0.274286 | 0.015551 | 25/5 |

| 1 | 0.850968 | 0.007508 | 0.620932 | 0.023824 | 0.290714 | 0.010996 | {'clf__max_depth': 5, 'clf__n_estimators': 50,... | 2.229425 | 0.844140 | 0.007473 | 0.609801 | 0.027459 | 0.272857 | 0.015085 | 50/5 |

| 2 | 0.855230 | 0.007315 | 0.627034 | 0.021852 | 0.292500 | 0.010850 | {'clf__max_depth': 5, 'clf__n_estimators': 100... | 4.209755 | 0.849065 | 0.011019 | 0.619450 | 0.026249 | 0.275000 | 0.016614 | 100/5 |

| 3 | 0.867271 | 0.006166 | 0.648583 | 0.012831 | 0.300714 | 0.010950 | {'clf__max_depth': 10, 'clf__n_estimators': 25... | 2.068099 | 0.865000 | 0.002259 | 0.651858 | 0.020059 | 0.285357 | 0.012305 | 25/10 |

| 4 | 0.869225 | 0.007955 | 0.655050 | 0.014192 | 0.300000 | 0.012495 | {'clf__max_depth': 10, 'clf__n_estimators': 50... | 3.791683 | 0.871323 | 0.004542 | 0.659386 | 0.021993 | 0.286786 | 0.015531 | 50/10 |

| 5 | 0.874949 | 0.011903 | 0.664613 | 0.014215 | 0.303214 | 0.013030 | {'clf__max_depth': 10, 'clf__n_estimators': 10... | 7.230055 | 0.872388 | 0.005256 | 0.663481 | 0.024010 | 0.286429 | 0.017627 | 100/10 |

| 6 | 0.853581 | 0.014851 | 0.660131 | 0.013713 | 0.296429 | 0.012016 | {'clf__max_depth': 20, 'clf__n_estimators': 25... | 3.181439 | 0.869824 | 0.005664 | 0.680407 | 0.016981 | 0.285357 | 0.014962 | 25/20 |

| 7 | 0.862653 | 0.016004 | 0.673352 | 0.011485 | 0.297143 | 0.013439 | {'clf__max_depth': 20, 'clf__n_estimators': 50... | 6.027631 | 0.876311 | 0.006772 | 0.690434 | 0.019828 | 0.287143 | 0.016506 | 50/20 |

| 8 | 0.870378 | 0.016910 | 0.677675 | 0.011698 | 0.299286 | 0.013190 | {'clf__max_depth': 20, 'clf__n_estimators': 10... | 11.521331 | 0.879728 | 0.006367 | 0.694063 | 0.020657 | 0.288571 | 0.016690 | 100/20 |

| 9 | 0.858527 | 0.008786 | 0.651899 | 0.009478 | 0.296429 | 0.010996 | {'clf__max_depth': 50, 'clf__n_estimators': 25... | 3.340531 | 0.869956 | 0.003717 | 0.674013 | 0.021356 | 0.283929 | 0.016671 | 25/50 |

| 10 | 0.865997 | 0.013420 | 0.663305 | 0.009296 | 0.296071 | 0.011401 | {'clf__max_depth': 50, 'clf__n_estimators': 50... | 6.319636 | 0.875154 | 0.003631 | 0.683127 | 0.020882 | 0.287143 | 0.015518 | 50/50 |

| 11 | 0.870256 | 0.014185 | 0.671611 | 0.011290 | 0.298571 | 0.013363 | {'clf__max_depth': 50, 'clf__n_estimators': 10... | 12.293192 | 0.878369 | 0.002908 | 0.691405 | 0.019560 | 0.287500 | 0.015199 | 100/50 |

The get_summary_performances function gives the summary of the best parameters and corresponding performances.

summary_performances_rf=get_summary_performances(performances_df_rf, parameter_column_name="Parameters summary")

summary_performances_rf

| AUC ROC | Average precision | Card Precision@100 | |

|---|---|---|---|

| Best estimated parameters | 100/20 | 100/20 | 100/20 |

| Validation performance | 0.88+/-0.01 | 0.694+/-0.02 | 0.289+/-0.02 |

| Test performance | 0.87+/-0.02 | 0.678+/-0.01 | 0.299+/-0.01 |

| Optimal parameters | 100/10 | 100/20 | 100/10 |

| Optimal test performance | 0.875+/-0.01 | 0.678+/-0.01 | 0.303+/-0.01 |

The best performances are obtained with forests containing 100 trees, with a maximum depth of 10 or 20. The optimal parameters differ from the best estimated parameters for the AUC and CP@100. The difference in terms of performances is however low, and the best estimated parameters can be considered close to the optimal ones.

The visualization of the performances as a function of the model parameters is trickier since two parameters are varied. Let us first fix the number of trees, and then vary the maximum tree depth.

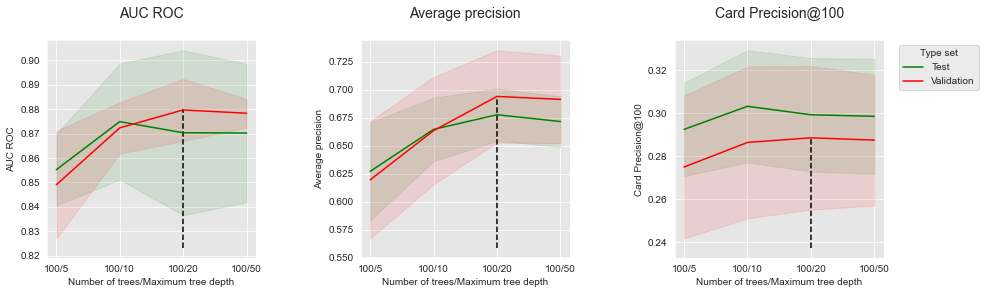

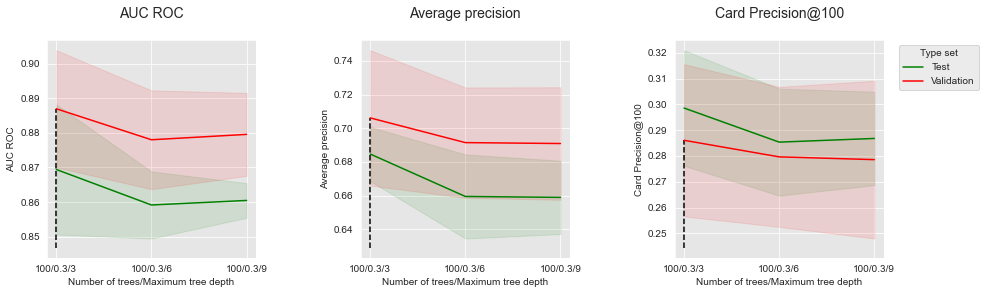

Fixing the number of trees to 100, we get:

performances_df_rf_fixed_number_of_trees=performances_df_rf[performances_df_rf["Parameters summary"].str.startswith("100")]

summary_performances_fixed_number_of_trees=get_summary_performances(performances_df_rf_fixed_number_of_trees, parameter_column_name="Parameters summary")

get_performances_plots(performances_df_rf_fixed_number_of_trees,

performance_metrics_list=['AUC ROC', 'Average precision', 'Card Precision@100'],

expe_type_list=['Test','Validation'], expe_type_color_list=['#008000','#FF0000'],

parameter_name="Number of trees/Maximum tree depth",

summary_performances=summary_performances_fixed_number_of_trees)

A maximum tree depth of 5 provides the lowest peformances. Performances increase with maximum tree depth, until a tree depth of 10 to 20 where they reach a plateau then slightly decrease.

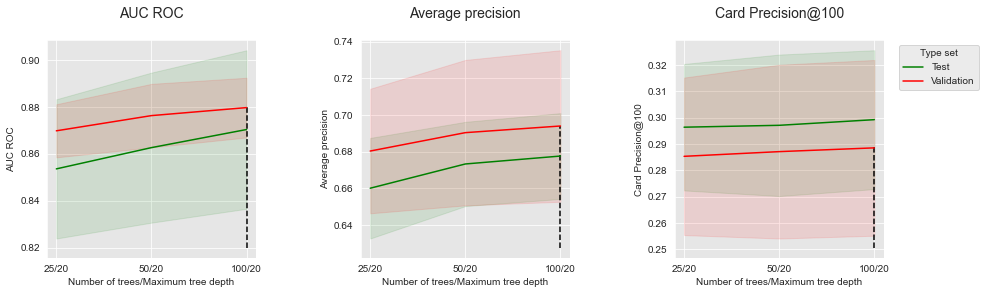

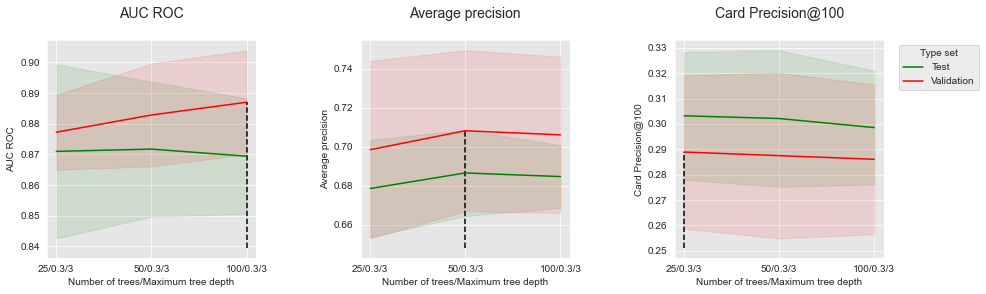

Let us then fix the maximum tree depth, and the vary the number of estimators. Fixing the maximum tree depth to 20, we get:

performances_df_rf_fixed_max_tree_depth=performances_df_rf[performances_df_rf["Parameters summary"].str.endswith("20")]

summary_performances_fixed_max_tree_depth=get_summary_performances(performances_df_rf_fixed_max_tree_depth, parameter_column_name="Parameters summary")

get_performances_plots(performances_df_rf_fixed_max_tree_depth,

performance_metrics_list=['AUC ROC', 'Average precision', 'Card Precision@100'],

expe_type_list=['Test','Validation'], expe_type_color_list=['#008000','#FF0000'],

parameter_name="Number of trees/Maximum tree depth",

summary_performances=summary_performances_fixed_max_tree_depth)

For all performance metrics, the common trend is an increase in performances as the number of trees is increased. The added performance gains however decrease with the number of added trees.

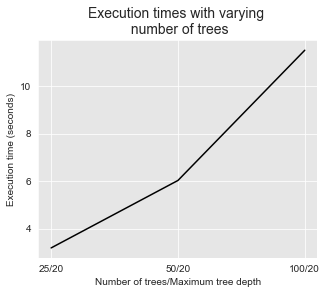

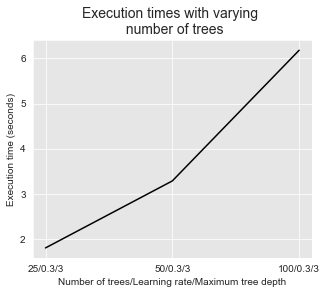

It is worth noting that the execution times for training random forests linearly increases with the number of trees. This can be illustrated by plotting the execution times as a function of the number of trees.

# Get the performance plot for a single performance metric

def get_execution_times_plot(performances_df,

title="",

parameter_name="Tree maximum depth"):

fig, ax = plt.subplots(1,1, figsize=(5,4))

# Plot data on graph

ax.plot(performances_df['Parameters summary'], performances_df["Execution time"],

color="black")

# Set title, and x and y axes labels

ax.set_title(title, fontsize=14)

ax.set(xlabel = parameter_name, ylabel="Execution time (seconds)")

get_execution_times_plot(performances_df_rf_fixed_max_tree_depth,

title="Execution times with varying \n number of trees",

parameter_name="Number of trees/Maximum tree depth")

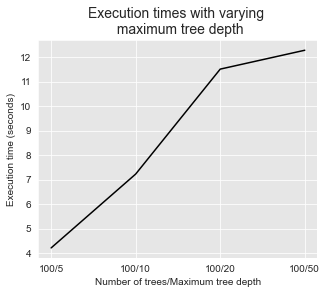

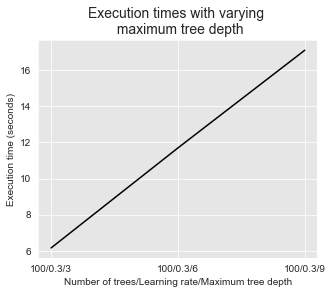

The execution times also increases with the maximum tree depth, as illustrated below.

get_execution_times_plot(performances_df_rf_fixed_number_of_trees,

title="Execution times with varying \n maximum tree depth",

parameter_name="Number of trees/Maximum tree depth")

All in all, the model selection procedure above took about 10 minutes to complete on one core, although only a small number of parameter combinations were tested (12 in total: 4 different parameters for the maximum tree depth, and 3 different parameters for the number of trees).

print("Total execution time for the model selection procedure: "+str(round(execution_time_rf,2))+"s")

Total execution time for the model selection procedure: 586.96s

This toy example illustrates the trade-off between performance and computation times in the search for optimal parameters. Computational resources are usually constrained, and one must carefully consider which hyperparameter combinations can be tested given the available resources.

3.2.3. XGBoost¶

XGBoost is a powerful learning algorithm whose tuning however relies on many hyperparameters. The most important ones are arguably the tree maximum depth (max_depth), the number of trees (n_estimtors), and the learning rate (learning_rate). By default, the maximum tree depth is set to 6, the number of trees to 100, and the learning rate to 0.3. Let us try other combinations, with max_depth in the set [3,6,9], n_estimators in the set [25,10,100], and learning_rate in the set [0.1, 0.3].

classifier = xgboost.XGBClassifier()

parameters = {'clf__max_depth':[3,6,9], 'clf__n_estimators':[25,50,100], 'clf__learning_rate':[0.1, 0.3],

'clf__random_state':[0], 'clf__n_jobs':[1], 'clf__verbosity':[0]}

start_time=time.time()

performances_df=model_selection_wrapper(transactions_df, classifier,

input_features, output_feature,

parameters, scoring,

start_date_training_for_valid,

start_date_training_for_test,

n_folds=n_folds,

delta_train=delta_train,

delta_delay=delta_delay,

delta_assessment=delta_assessment,

performance_metrics_list_grid=performance_metrics_list_grid,

performance_metrics_list=performance_metrics_list,

n_jobs=1)

execution_time_boosting = time.time()-start_time

parameters_dict=dict(performances_df['Parameters'])

performances_df['Parameters summary']=[str(parameters_dict[i]['clf__n_estimators'])+

'/'+

str(parameters_dict[i]['clf__learning_rate'])+

'/'+

str(parameters_dict[i]['clf__max_depth'])

for i in range(len(parameters_dict))]

# Rename to performances_df_xgboost for model performance comparison at the end of this notebook

performances_df_xgboost=performances_df

performances_df_xgboost

| AUC ROC Test | AUC ROC Test Std | Average precision Test | Average precision Test Std | Card Precision@100 Test | Card Precision@100 Test Std | Parameters | Execution time | AUC ROC Validation | AUC ROC Validation Std | Average precision Validation | Average precision Validation Std | Card Precision@100 Validation | Card Precision@100 Validation Std | Parameters summary | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 0.833094 | 0.012257 | 0.635603 | 0.022225 | 0.296071 | 0.014859 | {'clf__learning_rate': 0.1, 'clf__max_depth': ... | 2.740516 | 0.825157 | 0.009026 | 0.617990 | 0.025069 | 0.278214 | 0.015563 | 25/0.1/3 |

| 1 | 0.864766 | 0.006604 | 0.666130 | 0.012722 | 0.301429 | 0.013439 | {'clf__learning_rate': 0.1, 'clf__max_depth': ... | 4.426460 | 0.863627 | 0.003203 | 0.651369 | 0.030279 | 0.280714 | 0.014932 | 50/0.1/3 |

| 2 | 0.870792 | 0.012352 | 0.694030 | 0.008394 | 0.303929 | 0.012305 | {'clf__learning_rate': 0.1, 'clf__max_depth': ... | 7.717508 | 0.878438 | 0.009221 | 0.705235 | 0.019756 | 0.288214 | 0.015694 | 100/0.1/3 |

| 3 | 0.835862 | 0.012705 | 0.638601 | 0.025984 | 0.297500 | 0.014928 | {'clf__learning_rate': 0.1, 'clf__max_depth': ... | 4.346976 | 0.843097 | 0.014918 | 0.640099 | 0.026283 | 0.278571 | 0.015551 | 25/0.1/6 |

| 4 | 0.871589 | 0.014202 | 0.686221 | 0.012026 | 0.301786 | 0.009603 | {'clf__learning_rate': 0.1, 'clf__max_depth': ... | 8.303945 | 0.869654 | 0.002863 | 0.699780 | 0.016875 | 0.288214 | 0.016884 | 50/0.1/6 |

| 5 | 0.871278 | 0.011437 | 0.685991 | 0.008947 | 0.298571 | 0.010351 | {'clf__learning_rate': 0.1, 'clf__max_depth': ... | 17.992388 | 0.881340 | 0.004587 | 0.706922 | 0.017461 | 0.286429 | 0.017217 | 100/0.1/6 |

| 6 | 0.852550 | 0.003171 | 0.656631 | 0.012632 | 0.302857 | 0.012164 | {'clf__learning_rate': 0.1, 'clf__max_depth': ... | 4.437036 | 0.854345 | 0.008599 | 0.656910 | 0.023964 | 0.281429 | 0.012817 | 25/0.1/9 |

| 7 | 0.867596 | 0.016111 | 0.681919 | 0.011871 | 0.300000 | 0.009949 | {'clf__learning_rate': 0.1, 'clf__max_depth': ... | 9.128478 | 0.875070 | 0.006199 | 0.700656 | 0.018366 | 0.285714 | 0.015779 | 50/0.1/9 |

| 8 | 0.862519 | 0.007472 | 0.674149 | 0.007838 | 0.293929 | 0.012428 | {'clf__learning_rate': 0.1, 'clf__max_depth': ... | 18.618342 | 0.879667 | 0.003782 | 0.700592 | 0.017885 | 0.285000 | 0.017394 | 100/0.1/9 |

| 9 | 0.870988 | 0.014197 | 0.678544 | 0.012501 | 0.303214 | 0.012592 | {'clf__learning_rate': 0.3, 'clf__max_depth': ... | 1.809805 | 0.877231 | 0.006120 | 0.698490 | 0.022835 | 0.288929 | 0.015131 | 25/0.3/3 |

| 10 | 0.871726 | 0.010990 | 0.686534 | 0.011086 | 0.302143 | 0.013458 | {'clf__learning_rate': 0.3, 'clf__max_depth': ... | 3.290658 | 0.882839 | 0.008380 | 0.708226 | 0.020697 | 0.287500 | 0.016331 | 50/0.3/3 |

| 11 | 0.869414 | 0.009418 | 0.684661 | 0.008058 | 0.298571 | 0.011203 | {'clf__learning_rate': 0.3, 'clf__max_depth': ... | 6.179205 | 0.886993 | 0.008474 | 0.706116 | 0.020094 | 0.286071 | 0.014756 | 100/0.3/3 |

| 12 | 0.868900 | 0.010737 | 0.682132 | 0.008824 | 0.299286 | 0.011974 | {'clf__learning_rate': 0.3, 'clf__max_depth': ... | 3.157807 | 0.880707 | 0.005706 | 0.703211 | 0.016174 | 0.285000 | 0.015336 | 25/0.3/6 |

| 13 | 0.867046 | 0.011363 | 0.673906 | 0.007436 | 0.293929 | 0.009968 | {'clf__learning_rate': 0.3, 'clf__max_depth': ... | 6.032546 | 0.879301 | 0.008605 | 0.697563 | 0.016872 | 0.283571 | 0.016614 | 50/0.3/6 |

| 14 | 0.859138 | 0.004852 | 0.659458 | 0.012488 | 0.285357 | 0.010369 | {'clf__learning_rate': 0.3, 'clf__max_depth': ... | 11.699445 | 0.878025 | 0.007150 | 0.691442 | 0.016375 | 0.279643 | 0.013567 | 100/0.3/6 |

| 15 | 0.863341 | 0.007757 | 0.675966 | 0.008870 | 0.294286 | 0.011995 | {'clf__learning_rate': 0.3, 'clf__max_depth': ... | 4.462973 | 0.876948 | 0.004011 | 0.699722 | 0.017653 | 0.283571 | 0.015924 | 25/0.3/9 |

| 16 | 0.859114 | 0.003609 | 0.660666 | 0.008002 | 0.288214 | 0.008943 | {'clf__learning_rate': 0.3, 'clf__max_depth': ... | 8.684047 | 0.876392 | 0.006354 | 0.692759 | 0.017801 | 0.280357 | 0.014441 | 50/0.3/9 |

| 17 | 0.860454 | 0.002511 | 0.658901 | 0.010897 | 0.286786 | 0.009056 | {'clf__learning_rate': 0.3, 'clf__max_depth': ... | 17.091203 | 0.879577 | 0.006008 | 0.690895 | 0.016712 | 0.278571 | 0.015286 | 100/0.3/9 |

The get_summary_performances function gives the summary of the best parameters and corresponding performances.

summary_performances_xgboost=get_summary_performances(performances_df_xgboost, parameter_column_name="Parameters summary")

summary_performances_xgboost

| AUC ROC | Average precision | Card Precision@100 | |

|---|---|---|---|

| Best estimated parameters | 100/0.3/3 | 50/0.3/3 | 25/0.3/3 |

| Validation performance | 0.887+/-0.01 | 0.708+/-0.02 | 0.289+/-0.02 |

| Test performance | 0.869+/-0.01 | 0.687+/-0.01 | 0.303+/-0.01 |

| Optimal parameters | 50/0.3/3 | 100/0.1/3 | 100/0.1/3 |

| Optimal test performance | 0.872+/-0.01 | 0.694+/-0.01 | 0.304+/-0.01 |

The best parameters obtained by validation are the same for ROC AUC, and slightly differ for the average precision and CP@100. The corresponding test performances are however on par.

Let us plot the performances as a function of the maximum tree depth, for a number of trees set to 100. Increasing the maximum tree depth does not clearly affect the performances. It slightly increases performances for AUC ROC and AP, but slightly decreases it for CP@100.

performances_df_xgboost_fixed_number_of_trees=performances_df_xgboost[performances_df_xgboost["Parameters summary"].str.startswith("100/0.3")]

summary_performances_fixed_number_of_trees=get_summary_performances(performances_df_xgboost_fixed_number_of_trees, parameter_column_name="Parameters summary")

get_performances_plots(performances_df_xgboost_fixed_number_of_trees,

performance_metrics_list=['AUC ROC', 'Average precision', 'Card Precision@100'],

expe_type_list=['Test','Validation'], expe_type_color_list=['#008000','#FF0000'],

parameter_name="Number of trees/Maximum tree depth",

summary_performances=summary_performances_fixed_number_of_trees)

Let us then plot the performances as a function of the number of trees, for a maximum tree depth set to 5.

performances_df_xgboost_fixed_max_tree_depth=performances_df_xgboost[performances_df_xgboost["Parameters summary"].str.endswith("0.3/3")]

summary_performances_fixed_max_tree_depth=get_summary_performances(performances_df_xgboost_fixed_max_tree_depth, parameter_column_name="Parameters summary")

get_performances_plots(performances_df_xgboost_fixed_max_tree_depth,

performance_metrics_list=['AUC ROC', 'Average precision', 'Card Precision@100'],

expe_type_list=['Test','Validation'], expe_type_color_list=['#008000','#FF0000'],

parameter_name="Number of trees/Maximum tree depth",

summary_performances=summary_performances_fixed_max_tree_depth)

Increasing the number of trees from 25 to 50 allow to increase the performances for all performance metrics. Adding more trees however only provides slightly higher performances for AUC ROC and AP, and slightly decreases performances for CP@100.

Similar to random forests, increasing the maximum tree depth and the number of trees comes at a cost in terms of execution times. This is illustrated in the two figures below.

get_execution_times_plot(performances_df_xgboost_fixed_max_tree_depth,

title="Execution times with varying \n number of trees",

parameter_name="Number of trees/Learning rate/Maximum tree depth")

get_execution_times_plot(performances_df_xgboost_fixed_number_of_trees,

title="Execution times with varying \n maximum tree depth",

parameter_name="Number of trees/Learning rate/Maximum tree depth")

The total execution time was more than 10 minutes using one core.

print("Total execution time for the model selection procedure: "+str(round(execution_time_boosting,2))+"s")

Total execution time for the model selection procedure: 1251.2s

3.3. Comparison of model performances¶

The previous section detailed the performances of different model classes. Let us compare these performances in order to determine which model class provides the best performances.

For each model class, let us retrieve the performance for three types of parameters:

Default parameters: Default parameters that

sklearngives to a model class. The default parameters for each model class are:Decision tree:

max_depth=None.Logistic regression:

C=1.Random forest:

n_estimators=100,max_depth=None.XGBoost:

n_estimators=100,max_depth=6,learning_rate=0.3.

Best estimated parameters: Parameters that provide the highest performances on the validation set.

Optimal parameters: Parameters that provide the highest performances on the test set.

The model_selection_performances function below takes a dictionary of performance DataFrames and a performance metric, and retrieves the corresponding performances (mean together with standard deviation).

performances_df_dictionary={

"Decision Tree": performances_df_dt,

"Logistic Regression": performances_df_lr,

"Random Forest": performances_df_rf,

"XGBoost": performances_df_xgboost

}

def model_selection_performances(performances_df_dictionary,

performance_metric='AUC ROC',

model_classes=['Decision Tree',

'Logistic Regression',

'Random Forest',

'XGBoost'],

default_parameters_dictionary={

"Decision Tree": 50,

"Logistic Regression": 1,

"Random Forest": "100/50",

"XGBoost": "100/0.3/6"

}):

mean_performances_dictionary={

"Default parameters": [],

"Best validation parameters": [],

"Optimal parameters": []

}

std_performances_dictionary={

"Default parameters": [],

"Best validation parameters": [],

"Optimal parameters": []

}

# For each model class

for model_class in model_classes:

performances_df=performances_df_dictionary[model_class]

# Get the performances for the default paramaters

default_performances=performances_df[performances_df['Parameters summary']==default_parameters_dictionary[model_class]]

default_performances=default_performances.round(decimals=3)

mean_performances_dictionary["Default parameters"].append(default_performances[performance_metric+" Test"].values[0])

std_performances_dictionary["Default parameters"].append(default_performances[performance_metric+" Test Std"].values[0])

# Get the performances for the best estimated parameters

performances_summary=get_summary_performances(performances_df, parameter_column_name="Parameters summary")

mean_std_performances=performances_summary.loc[["Test performance"]][performance_metric].values[0]

mean_std_performances=mean_std_performances.split("+/-")

mean_performances_dictionary["Best validation parameters"].append(float(mean_std_performances[0]))

std_performances_dictionary["Best validation parameters"].append(float(mean_std_performances[1]))

# Get the performances for the boptimal parameters

mean_std_performances=performances_summary.loc[["Optimal test performance"]][performance_metric].values[0]

mean_std_performances=mean_std_performances.split("+/-")

mean_performances_dictionary["Optimal parameters"].append(float(mean_std_performances[0]))

std_performances_dictionary["Optimal parameters"].append(float(mean_std_performances[1]))

# Return the mean performances and their standard deviations

return (mean_performances_dictionary,std_performances_dictionary)

For examples, executing the function for the AUC ROC metric returns:

model_selection_performances(performances_df_dictionary,

performance_metric='AUC ROC')

({'Default parameters': [0.797, 0.868, 0.87, 0.859],

'Best validation parameters': [0.797, 0.868, 0.87, 0.869],

'Optimal parameters': [0.813, 0.868, 0.875, 0.872]},

{'Default parameters': [0.005, 0.015, 0.014, 0.005],

'Best validation parameters': [0.01, 0.02, 0.02, 0.01],

'Optimal parameters': [0.01, 0.02, 0.01, 0.01]})

For better visualization, let us plot the performances for the four model classes and for each performance metric as bar charts. The implementation is provided with the get_model_selection_performance_plot and get_model_selection_performances_plots below.

# Get the performance plot for a single performance metric

def get_model_selection_performance_plot(performances_df_dictionary,

ax,

performance_metric,

ylim=[0,1],

model_classes=['Decision Tree',

'Logistic Regression',

'Random Forest',

'XGBoost']):

(mean_performances_dictionary,std_performances_dictionary) = \

model_selection_performances(performances_df_dictionary=performances_df_dictionary,

performance_metric=performance_metric)

# width of the bars

barWidth = 0.3

# The x position of bars

r1 = np.arange(len(model_classes))

r2 = r1+barWidth

r3 = r1+2*barWidth

# Create Default parameters bars (Orange)

ax.bar(r1, mean_performances_dictionary['Default parameters'],

width = barWidth, color = '#CA8035', edgecolor = 'black',

yerr=std_performances_dictionary['Default parameters'], capsize=7, label='Default parameters')

# Create Best validation parameters bars (Red)

ax.bar(r2, mean_performances_dictionary['Best validation parameters'],

width = barWidth, color = '#008000', edgecolor = 'black',

yerr=std_performances_dictionary['Best validation parameters'], capsize=7, label='Best validation parameters')

# Create Optimal parameters bars (Green)

ax.bar(r3, mean_performances_dictionary['Optimal parameters'],

width = barWidth, color = '#2F4D7E', edgecolor = 'black',

yerr=std_performances_dictionary['Optimal parameters'], capsize=7, label='Optimal parameters')

# Set title, and x and y axes labels

ax.set_ylim(ylim[0],ylim[1])

ax.set_xticks(r2+barWidth/2)

ax.set_xticklabels(model_classes, rotation = 45, ha="right", fontsize=12)

ax.set_title(performance_metric+'\n', fontsize=18)

ax.set_xlabel("Model class", fontsize=16)

ax.set_ylabel(performance_metric, fontsize=15)

def get_model_selection_performances_plots(performances_df_dictionary,

performance_metrics_list=['AUC ROC', 'Average precision', 'Card Precision@100'],

ylim_list=[[0.6,0.9],[0.2,0.8],[0.2,0.35]],

model_classes=['Decision Tree',

'Logistic Regression',

'Random Forest',

'XGBoost']):

# Create as many graphs as there are performance metrics to display

n_performance_metrics = len(performance_metrics_list)

fig, ax = plt.subplots(1, n_performance_metrics, figsize=(5*n_performance_metrics,4))

parameter_types=['Default parameters','Best validation parameters','Optimal parameters']

# Plot performance metric for each metric in performance_metrics_list

for i in range(n_performance_metrics):

get_model_selection_performance_plot(performances_df_dictionary,

ax[i],

performance_metrics_list[i],

ylim=ylim_list[i],

model_classes=model_classes

)

ax[n_performance_metrics-1].legend(loc='upper left',

labels=parameter_types,

bbox_to_anchor=(1.05, 1),

title="Parameter type",

prop={'size': 12},

title_fontsize=12)

plt.subplots_adjust(wspace=0.5,

hspace=0.8)

This gives:

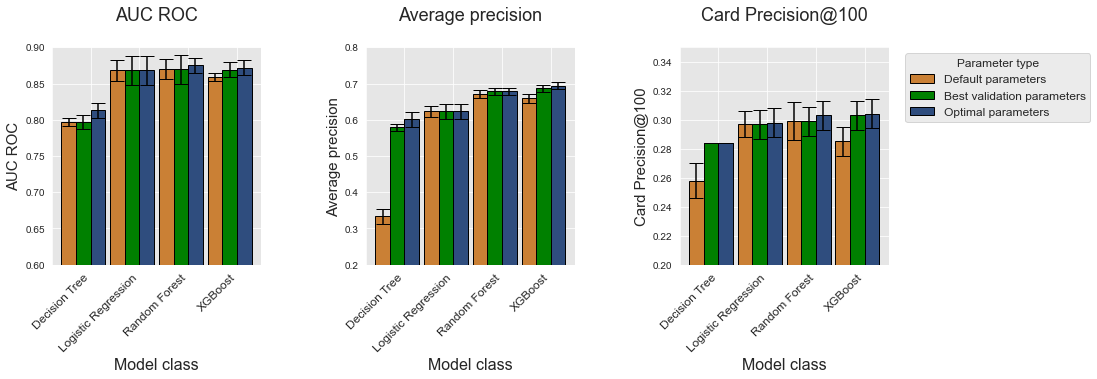

get_model_selection_performances_plots(performances_df_dictionary,

performance_metrics_list=['AUC ROC', 'Average precision', 'Card Precision@100'])

On this simulated dataset, XGBoost provides the highest performances in terms of Average Precision and CP@100, followed by random forest, logistic regression, and finally decision trees which have the lowest performances. The gap in terms of performance is most visible with the average precision metric. The performances of logistic regression, random forest, and XGBoost are very similar in terms of AUC ROC.

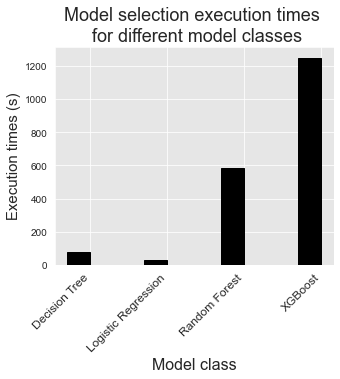

Let us plot the total execution times of the model selection procedure for each model class.

execution_times=[execution_time_dt,execution_time_lr,

execution_time_rf,execution_time_boosting]

%%capture

fig_model_selection_execution_times_for_each_model_class, ax = plt.subplots(1, 1, figsize=(5,4))

model_classes=['Decision Tree','Logistic Regression','Random Forest','XGBoost']

# width of the bars

barWidth = 0.3

# The x position of bars

r1 = np.arange(len(model_classes))

# Create execution times bars

ax.bar(r1, execution_times[0:4],

width = barWidth, color = 'black', edgecolor = 'black',

capsize=7)

ax.set_xticks(r1+barWidth/2)

ax.set_xticklabels(model_classes, rotation = 45, ha="right", fontsize=12)

ax.set_title('Model selection execution times \n for different model classes', fontsize=18)

ax.set_xlabel("Model class", fontsize=16)

ax.set_ylabel("Execution times (s)", fontsize=15)

fig_model_selection_execution_times_for_each_model_class

The comparison in terms of execution times is mostly qualitative since they depend to a large extent on the number of parameter combinations that were considered in the model selection procedure. It however illustrates that model selection for complex models such as random forests or boosting usually requires more computational resources, since they require tuning a higher number of hyperparameters.

3.4. Random search¶

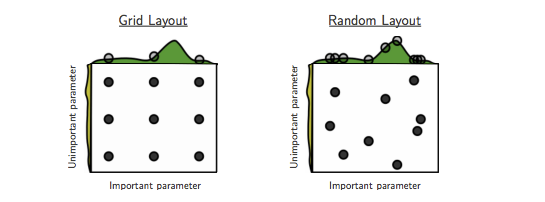

Grid search is a widely used strategy for hyperparameter optimization. It however quickly becomes intractable when the number of hyperparameters is high since the number of parameter combinations grows exponentially with the number of parameters.

An alternative to grid search is random search, where random combinations of parameters are assessed for a fixed number of combinations. Besides allowing to limit the number of tested parameter combinations, random combinations have been shown both empirically and theoretically to be more efficient for hyperparameter optimization than grid search [BB12].

The intuition for the efficiency of random search is illustrated in Fig. 3. Essentially, random search allows to more efficiently explore the space of important hyperparameters.

The implementation of random search in sklearn can be performed by relying on RandomizedSearchCV instead of GridSearchCV in the prequential search. Let us modify the prequential_grid_search into a more generic prequential_parameters_search function, by adding three new parameters:

type_search: Either ‘grid’ for grid search, or ‘random’ for random search.n_iter: Number of iterations (parameter combinations) for the random search.random_state: Random state for reproducibility of the random search.

def prequential_parameters_search(transactions_df,

classifier,

input_features, output_feature,

parameters, scoring,

start_date_training,

n_folds=4,

expe_type='Test',

delta_train=7,

delta_delay=7,

delta_assessment=7,

performance_metrics_list_grid=['roc_auc'],

performance_metrics_list=['AUC ROC'],

type_search='grid',

n_iter=10,

random_state=0,

n_jobs=-1):

estimators = [('scaler', sklearn.preprocessing.StandardScaler()), ('clf', classifier)]

pipe = sklearn.pipeline.Pipeline(estimators)

prequential_split_indices=prequentialSplit(transactions_df,

start_date_training=start_date_training,

n_folds=n_folds,

delta_train=delta_train,

delta_delay=delta_delay,

delta_assessment=delta_assessment)

parameters_search = None

if type_search=="grid":

parameters_search = sklearn.model_selection.GridSearchCV(pipe, parameters, scoring=scoring, cv=prequential_split_indices,

refit=False, n_jobs=n_jobs)

if type_search=="random":

parameters_search = sklearn.model_selection.RandomizedSearchCV(pipe, parameters, scoring=scoring, cv=prequential_split_indices,

refit=False, n_jobs=n_jobs,n_iter=n_iter,random_state=random_state)

X=transactions_df[input_features]

y=transactions_df[output_feature]

parameters_search.fit(X, y)

performances_df=pd.DataFrame()

for i in range(len(performance_metrics_list_grid)):

performances_df[performance_metrics_list[i]+' '+expe_type]=parameters_search.cv_results_['mean_test_'+performance_metrics_list_grid[i]]

performances_df[performance_metrics_list[i]+' '+expe_type+' Std']=parameters_search.cv_results_['std_test_'+performance_metrics_list_grid[i]]

performances_df['Parameters']=parameters_search.cv_results_['params']

performances_df['Execution time']=parameters_search.cv_results_['mean_fit_time']

return performances_df

def model_selection_wrapper(transactions_df,

classifier,

input_features, output_feature,

parameters,

scoring,

start_date_training_for_valid,

start_date_training_for_test,

n_folds=4,

delta_train=7,

delta_delay=7,

delta_assessment=7,

performance_metrics_list_grid=['roc_auc'],

performance_metrics_list=['AUC ROC'],

type_search='grid',

n_iter=10,

random_state=0,

n_jobs=-1):

# Get performances on the validation set using prequential validation

performances_df_validation=prequential_parameters_search(transactions_df, classifier,

input_features, output_feature,

parameters, scoring,

start_date_training=start_date_training_for_valid,

n_folds=n_folds,

expe_type='Validation',

delta_train=delta_train,

delta_delay=delta_delay,

delta_assessment=delta_assessment,

performance_metrics_list_grid=performance_metrics_list_grid,

performance_metrics_list=performance_metrics_list,

type_search=type_search,

n_iter=n_iter,

random_state=random_state,

n_jobs=n_jobs)

# Get performances on the test set using prequential validation

performances_df_test=prequential_parameters_search(transactions_df, classifier,

input_features, output_feature,

parameters, scoring,

start_date_training=start_date_training_for_test,

n_folds=n_folds,

expe_type='Test',

delta_train=delta_train,

delta_delay=delta_delay,

delta_assessment=delta_assessment,

performance_metrics_list_grid=performance_metrics_list_grid,

performance_metrics_list=performance_metrics_list,

type_search=type_search,

n_iter=n_iter,

random_state=random_state,

n_jobs=n_jobs)

# Bind the two resulting DataFrames

performances_df_validation.drop(columns=['Parameters','Execution time'], inplace=True)

performances_df=pd.concat([performances_df_test,performances_df_validation],axis=1)

# And return as a single DataFrame

return performances_df

Let us rerun the model selection for boosting, but using random search, with 10 parameter combinations.

classifier = xgboost.XGBClassifier()

parameters = {'clf__max_depth':[3,6,9], 'clf__n_estimators':[25,50,100],'clf__learning_rate':[0.1,0.3],

'clf__random_state':[0],'clf__n_jobs':[1],'clf__n_verbosity':[0]}

start_time=time.time()

performances_df=model_selection_wrapper(transactions_df, classifier,

input_features, output_feature,

parameters, scoring,

start_date_training_for_valid,

start_date_training_for_test,

n_folds=n_folds,

delta_train=delta_train,

delta_delay=delta_delay,

delta_assessment=delta_assessment,

performance_metrics_list_grid=performance_metrics_list_grid,

performance_metrics_list=performance_metrics_list,

type_search='random',

n_iter=10,

random_state=0,

n_jobs=1)

execution_time_boosting_random = time.time()-start_time

parameters_dict=dict(performances_df['Parameters'])

performances_df['Parameters summary']=[str(parameters_dict[i]['clf__n_estimators'])+

'/'+

str(parameters_dict[i]['clf__learning_rate'])+

'/'+

str(parameters_dict[i]['clf__max_depth'])

for i in range(len(parameters_dict))]

# Rename to performances_df_xgboost_random for model performance comparison

performances_df_xgboost_random=performances_df

performances_df_xgboost_random

| AUC ROC Test | AUC ROC Test Std | Average precision Test | Average precision Test Std | Card Precision@100 Test | Card Precision@100 Test Std | Parameters | Execution time | AUC ROC Validation | AUC ROC Validation Std | Average precision Validation | Average precision Validation Std | Card Precision@100 Validation | Card Precision@100 Validation Std | Parameters summary | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 0.864766 | 0.006604 | 0.666130 | 0.012722 | 0.301429 | 0.013439 | {'clf__random_state': 0, 'clf__n_verbosity': 0... | 3.234625 | 0.863627 | 0.003203 | 0.651369 | 0.030279 | 0.280714 | 0.014932 | 50/0.1/3 |

| 1 | 0.852550 | 0.003171 | 0.656631 | 0.012632 | 0.302857 | 0.012164 | {'clf__random_state': 0, 'clf__n_verbosity': 0... | 4.030167 | 0.854345 | 0.008599 | 0.656910 | 0.023964 | 0.281429 | 0.012817 | 25/0.1/9 |

| 2 | 0.862519 | 0.007472 | 0.674149 | 0.007838 | 0.293929 | 0.012428 | {'clf__random_state': 0, 'clf__n_verbosity': 0... | 17.273730 | 0.879667 | 0.003782 | 0.700592 | 0.017885 | 0.285000 | 0.017394 | 100/0.1/9 |

| 3 | 0.871726 | 0.010990 | 0.686534 | 0.011086 | 0.302143 | 0.013458 | {'clf__random_state': 0, 'clf__n_verbosity': 0... | 3.859597 | 0.882839 | 0.008380 | 0.708226 | 0.020697 | 0.287500 | 0.016331 | 50/0.3/3 |

| 4 | 0.859138 | 0.004852 | 0.659458 | 0.012488 | 0.285357 | 0.010369 | {'clf__random_state': 0, 'clf__n_verbosity': 0... | 13.659157 | 0.878025 | 0.007150 | 0.691442 | 0.016375 | 0.279643 | 0.013567 | 100/0.3/6 |

| 5 | 0.871589 | 0.014202 | 0.686221 | 0.012026 | 0.301786 | 0.009603 | {'clf__random_state': 0, 'clf__n_verbosity': 0... | 6.731956 | 0.869654 | 0.002863 | 0.699780 | 0.016875 | 0.288214 | 0.016884 | 50/0.1/6 |

| 6 | 0.870792 | 0.012352 | 0.694030 | 0.008394 | 0.303929 | 0.012305 | {'clf__random_state': 0, 'clf__n_verbosity': 0... | 7.344713 | 0.878438 | 0.009221 | 0.705235 | 0.019756 | 0.288214 | 0.015694 | 100/0.1/3 |

| 7 | 0.859114 | 0.003609 | 0.660666 | 0.008002 | 0.288214 | 0.008943 | {'clf__random_state': 0, 'clf__n_verbosity': 0... | 8.636219 | 0.876392 | 0.006354 | 0.692759 | 0.017801 | 0.280357 | 0.014441 | 50/0.3/9 |

| 8 | 0.860454 | 0.002511 | 0.658901 | 0.010897 | 0.286786 | 0.009056 | {'clf__random_state': 0, 'clf__n_verbosity': 0... | 18.037850 | 0.879577 | 0.006008 | 0.690895 | 0.016712 | 0.278571 | 0.015286 | 100/0.3/9 |

| 9 | 0.870988 | 0.014197 | 0.678544 | 0.012501 | 0.303214 | 0.012592 | {'clf__random_state': 0, 'clf__n_verbosity': 0... | 1.766806 | 0.877231 | 0.006120 | 0.698490 | 0.022835 | 0.288929 | 0.015131 | 25/0.3/3 |

The get_summary_performances function gives the summary of the best parameters and corresponding performances.

summary_performances_xgboost_random=get_summary_performances(performances_df_xgboost_random, parameter_column_name="Parameters summary")

summary_performances_xgboost_random

| AUC ROC | Average precision | Card Precision@100 | |

|---|---|---|---|

| Best estimated parameters | 50/0.3/3 | 50/0.3/3 | 25/0.3/3 |

| Validation performance | 0.883+/-0.01 | 0.708+/-0.02 | 0.289+/-0.02 |

| Test performance | 0.872+/-0.01 | 0.687+/-0.01 | 0.303+/-0.01 |

| Optimal parameters | 50/0.3/3 | 100/0.1/3 | 100/0.1/3 |

| Optimal test performance | 0.872+/-0.01 | 0.694+/-0.01 | 0.304+/-0.01 |

The performances are essentially the same as those obtained with the grid search.

# Performances with grid search

summary_performances_xgboost

| AUC ROC | Average precision | Card Precision@100 | |

|---|---|---|---|

| Best estimated parameters | 100/0.3/3 | 50/0.3/3 | 25/0.3/3 |

| Validation performance | 0.887+/-0.01 | 0.708+/-0.02 | 0.289+/-0.02 |

| Test performance | 0.869+/-0.01 | 0.687+/-0.01 | 0.303+/-0.01 |

| Optimal parameters | 50/0.3/3 | 100/0.1/3 | 100/0.1/3 |

| Optimal test performance | 0.872+/-0.01 | 0.694+/-0.01 | 0.304+/-0.01 |

The execution time was however significantly faster.

print("Total execution time for XGBoost with grid search: "+str(round(execution_time_boosting,2))+"s")

print("Total execution time for XGBoost with random search: "+str(round(execution_time_boosting_random,2))+"s")

Total execution time for XGBoost with grid search: 1251.2s

Total execution time for XGBoost with random search: 690.32s

3.5. Saving of results¶

Let us finally save the performance results and execution times.

performances_df_dictionary={

"Decision Tree": performances_df_dt,

"Logistic Regression": performances_df_lr,

"Random Forest": performances_df_rf,

"XGBoost": performances_df_xgboost,

"XGBoost Random": performances_df_xgboost_random

}

execution_times=[execution_time_dt,

execution_time_lr,

execution_time_rf,

execution_time_boosting,

execution_time_boosting_random]

Both data structures are saved as a Pickle file.

filehandler = open('performances_model_selection.pkl', 'wb')

pickle.dump((performances_df_dictionary, execution_times), filehandler)

filehandler.close()